It once seemed as if Fever-Tree (FEVR) could do no wrong. After years of explosive growth, during which consumers fell for its premium products and investors snapped up the shares, it became the largest company on Aim in 2019 – just five years after listing.

Bull points

- Double-digit revenue forecasts

- Market leader

Bear points

- Poor record of margin guidance

- Exposed to down-trading

- No price increases in US

- Heavily shorted

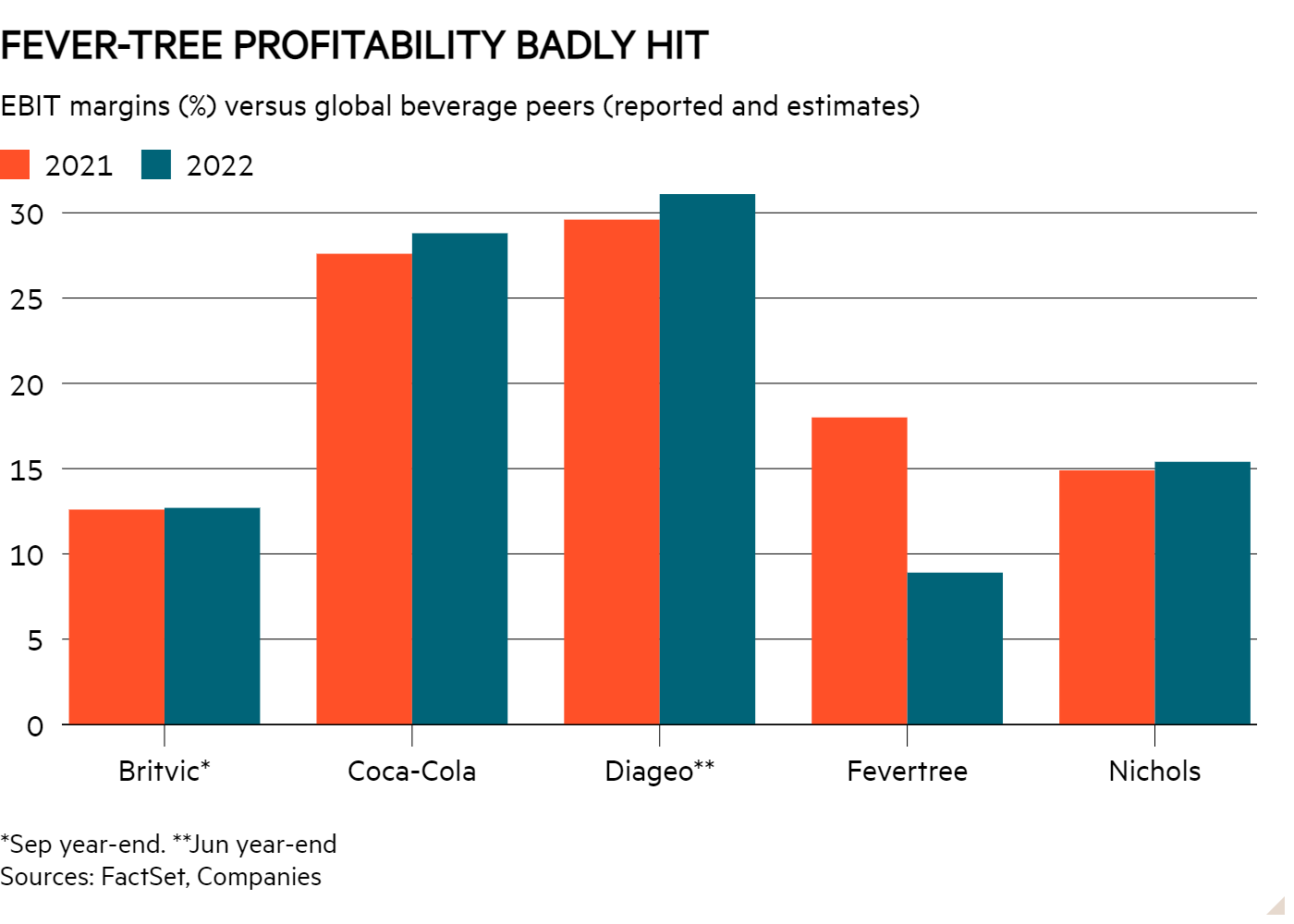

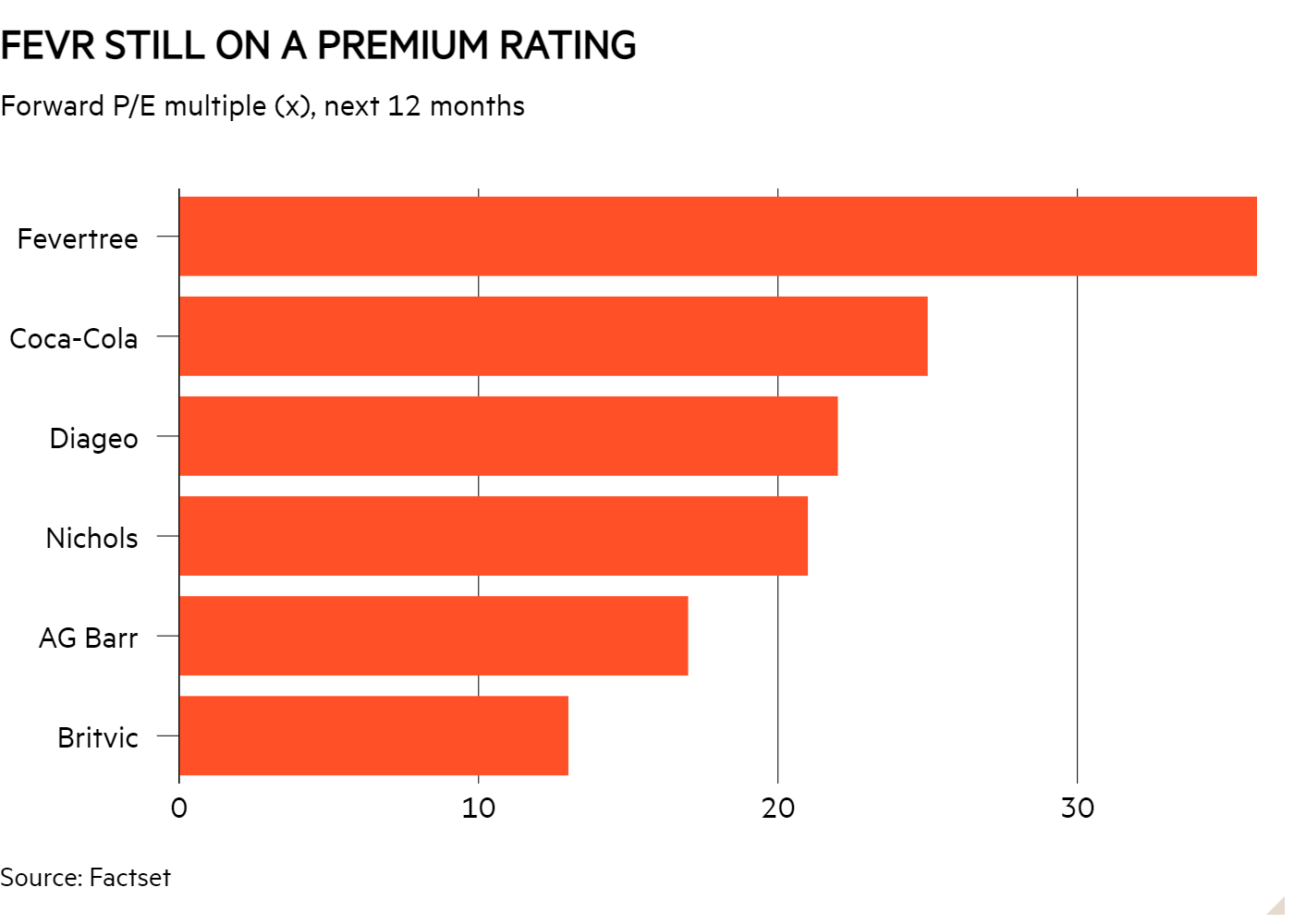

But both the immediate and longer-term outlooks seem increasingly cloudy. Buffeted by a range of headwinds, the supplier of high-end tonics and mixers is now an expensively rated company that consistently over-promises and fails to deliver on margin guidance and faces challenges across its markets which its operating model is ill-equipped to deal with. And a key warning sign, flashing red, is that its shares are the fourth most shorted in London.July’s pre-close trading update, released ahead of interim results due on 13 September, sent the shares plunging as the company warned of a “materially changed” outlook. Management pointed to labour shortages in the US, the knock-on exposure to high sea freight costs from having to ramp up production in the UK and send goods across the Atlantic, and the restricted availability of – and soaring costs of – glass.The result of these issues was another cut to gross margin guidance, this time taking expectations down 4 to 6 percentage points to a range of 33 to 35 per cent for the 2022 calendar year. If this was a one-off event it might be understandable, given the volatile economic backdrop, but Fever-Tree has now failed to hit its own margin guidance for a stonking six years on the trot. And a further profit warning didn’t help matters, with cash profit guidance chopped by over 36 per cent between the May and July updates. This doesn’t inspire confidence management’s analysis of future performance.The gloomy news sparked a very bearish note from RBC Capital Markets, whose analysts slashed their target price from £16 to £7, downgraded their recommendation to underperform (basically, a sell), and wrote of “potential for further margin downgrades”, “mounting headwinds threatening the top-line” and a lack of confidence in “what profitability Fever-Tree can achieve in the long-term as well as the short-term”. Ouch. Trading downThe sales performance for the half-year to 30 June was fairly robust, with uplifts across each of Fever-Tree’s markets. UK revenues rose 6 per cent to £54mn, the US edged up 11 per cent to £40mn, Europe grew 27 per cent to £52mn, while the rest of the world division (key markets are Australia and Canada) nudged up 7 per cent to £15mn. While the consensus analyst position is for Fever-Tree to achieve annual double-digit revenue growth over the next few years, the company looks at risk from the cost of living crisis as the economic outlook worsens and bills rise. This could weigh on growth.The nature of Fever-Tree’s higher-end product range is both a blessing and a curse. On the one hand, and in the past, it has tacked the company to trends around premiumisation and a growing global middle class drinking more mixed alcoholic drinks and willing to pay more for a “superior” product. Diageo (DGE) is a great example of a beverage sector peer which has gained from this, though it is helped by having a more flexible pricing range than Fever-Tree. But the elephant in the room for Fever-Tree is that its products are much pricier than other mixer options. This looks unhelpful as consumer cost pressures worsen significantly in the short to medium-term.We wrote in July about the trading down trend in the US beverage market highlighted by RBC and Deutsche Bank analysts, with warnings of a decline in spirits consumption amidst low-income consumers and falling spirits growth. But it looks like trading down could hurt Fever-Tree the most in the UK. RBC said that “there is very little further upside, and plenty of downside, when the consumer environment becomes increasingly difficult” in the company’s domestic market, given high penetration and pricing. While other markets have grown in importance for the business over recent years, the UK is still Fever-Tree’s biggest revenue contributor and any hit to volumes will be felt. American dream or nightmare?Continued growth and expansion into the US are key parts of the bull argument for Fever-Tree shares. There has been solid revenue progress in that market over the last couple of years, as the company battles it out with big competitors Schweppes and Canada Dry and smaller players in the premium space such as Fentimans and Q Mixers.According to data provider Nielsen, Fever-Tree could boast the market-leading retail tonic brand in the US at its latest year-end, and off-trade sales were up by 144 per cent for the 26 weeks to 18 June this year against 2019. Not bad, clearly. But there are serious questions over the level of profitability the company will be able to achieve stateside.Fever-Tree doesn’t disclose a lot of information about its US operations. But we do know it hasn’t increased US prices this year, and there have been no indications that it will do so. Given soaring inflation, this seems odd and feels like a missed opportunity – though perhaps this is because pricing for supermarkets (where most of its US sales are channeled) is more complex. Whatever the case, the company’s pricing power looks weak in the US and when more cents are eventually added on to the price tag volumes could be impacted.Peel Hunt thinks that cash profit margins in the US are currently in the low single-digits and will only reach 20 per cent in the long-term, far below the low-30s range that management aims for and consistently achieved by Schweppes distributor (and global beverages sector exemplar) Coca-Cola (US:KO). This won’t satisfy investors. The broker’s analysts expect Fever-Tree to be “a perennial price taker from its bottlers given its lack of scale”, in part due to what they see as “unconvincing” brand power in the Land of the Free.

Lack of cost controlAn issue the company can’t escape from in this inflationary period is an asset-light business model. Fever-Tree outsources much of its production and logistics. Bottling, for example, is handled by third parties. In good times, this model can help keep fixed costs low. But in an environment of soaring costs and disrupted supply chains, the company looks exposed.Goodbody analysts said that the company’s structure “has been a key enabler in scaling the brand in domestic and international markets” but that it leaves it “with less internal levers to mitigate cost pressures through internal efficiencies”.To this end, management’s claim in July’s update that “a number of significant cost impacts… will be transitory in nature”, though intended as reassuring, seems dubious. Costs are rising, few economists see a clear off-ramp for inflation, and the company hasn’t hedged its energy exposure. And given its small size compared to peers, bottling suppliers are likely to put bigger contracts first. All of this means Fever-Tree has poor visibility over costs and a lack of control over the logistical difficulties which are impacting margins and profits. A premium share price, tooOnce this ugly cocktail is mixed, it’s hard to make the case for Fever-Tree shares. Though the stock has fallen by almost 70 per cent in 2022, the rating hasn’t come down far enough in our view. On 34 times’ FactSet-compiled consensus forward earnings for 2023, the company trades at a significant premium to the wider beverage sector. It is also a third higher than Coca-Cola, which despite its thinner long-term growth profile has a longer and more consistent track record of margin guidance, cost control and capital allocation, as well as the world’s most valuable drinks brand.

Fever-Tree is a homegrown success story that’s hard not to admire. But that story has gone flat. Investors betting that some fizz can return to the shares anytime soon may well find the taste gets a lot more bitter first.Company DetailsNameMkt CapPrice52-Wk Hi/LoFevertree Drinks (FEVR)£1.05bn905p2,871p / 805pSize/DebtNAV per share*Net Cash / Debt(-)Net Debt / EbitdaOp Cash/ Ebitda242p£163m-95%ValuationFwd PE (+12mths)Fwd DY (+12mths)FCF yld (+12mths)P/Sales361.5%2.5%3.4Quality/ GrowthEBIT MarginROCE5yr Sales CAGR5yr EPS CAGR18.0%20.7%24.9%9.9%Forecasts/ MomentumFwd EPS grth NTMFwd EPS grth STM3-mth Mom3-mth Fwd EPS change%-45%28%-42.5%-42.1%Year End 31 DecSales (£mn)Profit before tax (£mn)EPS (p)DPS (p)201926172.951.114.9202025251.636.715.7202131156.039.715.7f’cst 202235732.021.813.8f’cst 202339840.526.515.3chg (%)+11+27+22+11Source: FactSet, adjusted PTP and EPS figuresNTM = Next 12 monthsSTM = Second 12 months (ie one year from now)

.

.jpg)