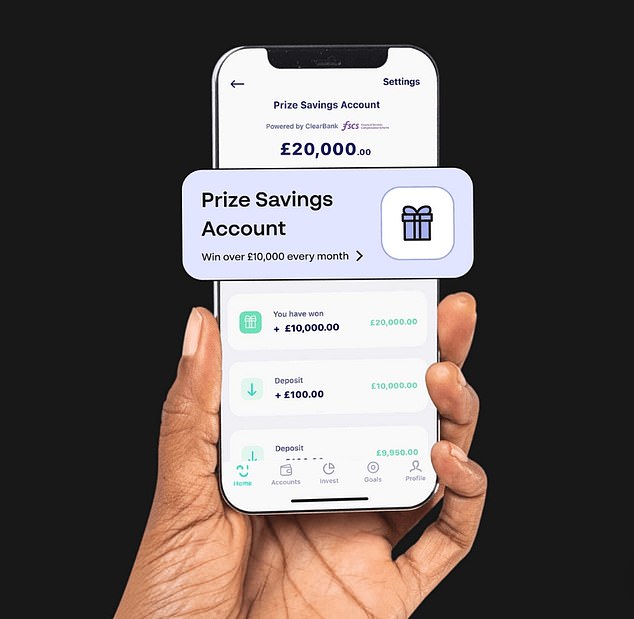

An app-based savings provider is offering its customers the chance to win monthly prizes in a similar vein to NS&I Premium Bonds.The Prize Savings Account, launched by savings and investing app, Chip, is an easy-access account giving savers the chance to win one prize of £10,000 as well as 250 smaller prizes of £10, each month.Savers will be entered into the monthly draw if they have at least £100 in their account at the end of each month.The minimum deposit into the account is £1 and the maximum amount is £85,000, with every £10 deposited counting as one entry per month.  Lottery style savings: Each month Chip randomly selects winners from all eligible entries.This means the more savers deposit, the more entries they have, up to a maximum of 8,500 entries per customer.Savers can also withdraw anytime with funds arriving in seconds, according to Chip – although in some cases it can take up to two hours.Chip is hoping its improved user experience and rapid withdrawal speed will appeal to Premium Bond holders who may be fed up with recent issues when accessing their cash.Last week, we reported how hundreds of savers were unable to access their savings accounts with NS&I due to its new online login system, three weeks after the issue was first reported.Simon Rabin, founder and chief executive of Chip pitched the new product as a genuine alternative to NS&I’s Premium Bonds.’It’s time for a more premium… Premium Bond,’ said Rabin, ‘we saw an opportunity to create a prize savings account with an amazing user experience.’NS&I Premium Bonds are a savings account you can put money into (and take out when you want), where the interest paid is decided by a monthly prize draw.’However, withdrawals sometimes take up to six days, and in December 2021 NS&I received 4,187 customer complaints that month.’What’s more, in late 2021 there was a whopping £74,452,325 in unclaimed prizes. We think when it comes to customer experience, there’s a lot of room for improvement – we think our new “Prize Savings Account” is just what you need.’Similar to Premium Bonds, Chip’s offering is a non-interest-bearing savings account provided by its partner bank, ClearBank.Any savings held in the account are protected by the Financial Services Compensation Scheme up to £85,000 per person.What is Chip?Chip is an automatic savings and investment app designed with the intention of helping its customers to save without having to think about it.Its app is available on iOS and Android and is used by over 500,000 people. In total it has more than £1billion in customer savings.Chip uses artificial intelligence technology linked to their bank account via open banking to calculate how much they can afford to save based on their spending habits.

Lottery style savings: Each month Chip randomly selects winners from all eligible entries.This means the more savers deposit, the more entries they have, up to a maximum of 8,500 entries per customer.Savers can also withdraw anytime with funds arriving in seconds, according to Chip – although in some cases it can take up to two hours.Chip is hoping its improved user experience and rapid withdrawal speed will appeal to Premium Bond holders who may be fed up with recent issues when accessing their cash.Last week, we reported how hundreds of savers were unable to access their savings accounts with NS&I due to its new online login system, three weeks after the issue was first reported.Simon Rabin, founder and chief executive of Chip pitched the new product as a genuine alternative to NS&I’s Premium Bonds.’It’s time for a more premium… Premium Bond,’ said Rabin, ‘we saw an opportunity to create a prize savings account with an amazing user experience.’NS&I Premium Bonds are a savings account you can put money into (and take out when you want), where the interest paid is decided by a monthly prize draw.’However, withdrawals sometimes take up to six days, and in December 2021 NS&I received 4,187 customer complaints that month.’What’s more, in late 2021 there was a whopping £74,452,325 in unclaimed prizes. We think when it comes to customer experience, there’s a lot of room for improvement – we think our new “Prize Savings Account” is just what you need.’Similar to Premium Bonds, Chip’s offering is a non-interest-bearing savings account provided by its partner bank, ClearBank.Any savings held in the account are protected by the Financial Services Compensation Scheme up to £85,000 per person.What is Chip?Chip is an automatic savings and investment app designed with the intention of helping its customers to save without having to think about it.Its app is available on iOS and Android and is used by over 500,000 people. In total it has more than £1billion in customer savings.Chip uses artificial intelligence technology linked to their bank account via open banking to calculate how much they can afford to save based on their spending habits.  Jackpot: Chip is offering one big grand prize each month worth £10,000. It then transfers that money from their current account to their Chip account – automatically whilst not interfering with a person’s normal day-to-day spending habits.Savers can also choose to set up a recurring payment, just like a direct debit that can be taken either weekly, fortnightly or monthly.The new account also allows savers to use both the auto-saves feature and the recurring payments to automatically deposit into the Prize Savings Account.Customers can increase or decrease the amount Chip puts aside by tweaking their saving level on the app, which determines how fast or slow they want to save.Chip can apparently adapt to a person overspending or earning irregular income and can adjust the savings amounts accordingly.It offers a host of features – it analyses your spending habits, helps set savings goals, and can automatically set a regular amount to save every time you get paid by your employer.How does its prize giving account compare?Chip may view disgruntled Premium Bond holders as its primary target. However, this will be no easy task given the amount of trust people have in the 65-year old savings product. NS&I’s draw has been running since 1956 and there are roughly 21million Premium Bond holders holding more than 118billion eligible £1 bonds between them.Chip is unable to offer the big money prizes that NS&I is, which will likely remove the magic for many.

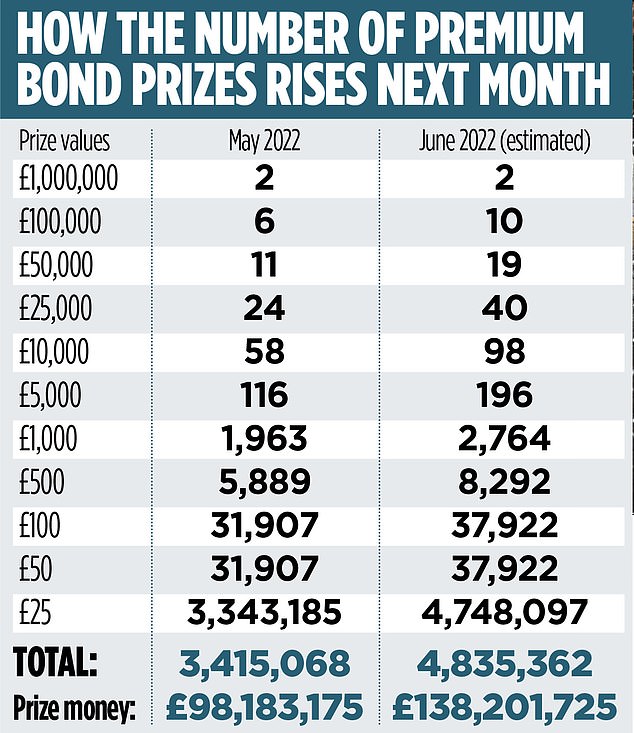

Jackpot: Chip is offering one big grand prize each month worth £10,000. It then transfers that money from their current account to their Chip account – automatically whilst not interfering with a person’s normal day-to-day spending habits.Savers can also choose to set up a recurring payment, just like a direct debit that can be taken either weekly, fortnightly or monthly.The new account also allows savers to use both the auto-saves feature and the recurring payments to automatically deposit into the Prize Savings Account.Customers can increase or decrease the amount Chip puts aside by tweaking their saving level on the app, which determines how fast or slow they want to save.Chip can apparently adapt to a person overspending or earning irregular income and can adjust the savings amounts accordingly.It offers a host of features – it analyses your spending habits, helps set savings goals, and can automatically set a regular amount to save every time you get paid by your employer.How does its prize giving account compare?Chip may view disgruntled Premium Bond holders as its primary target. However, this will be no easy task given the amount of trust people have in the 65-year old savings product. NS&I’s draw has been running since 1956 and there are roughly 21million Premium Bond holders holding more than 118billion eligible £1 bonds between them.Chip is unable to offer the big money prizes that NS&I is, which will likely remove the magic for many.  Premium Bonds have been a popular product for UK savers for more than 65 years.Although the majority of prizes are worth £25, Premium Bond holders are always in with a distant chance of winning one of the two £1million monthly jackpot prizes. There are also ten £100,000 prizes and 19 prizes worth £50,000.In May, NS&I increased the Premium Bond underlying prize fund rate from 1 per cent to 1.4 per cent boosting the chances of its 21million savers bagging a monthly prize.It means the odds of each £1 Premium Bond number winning a prize has now changed from 34,500 to 1 to 24,500 to 1. Chip is unable to give the odds of winning just yet as its only in the first month of the account being live, although it says in future, it hopes to share this once it collects more data. However, needless to say, the more savers deposit the more entries the will have in the prize draw each month.One other factors for savers to consider is the fact that Premium Bond prizes are tax free whilst Chip’s prizes could incur tax depending on whether they exceed a person’s annual tax free allowance. Ultimately, there is no guarantee of winning anything with these prize draws. Savers looking for guaranteed returns whilst retaining access to their cash may do better to consider an interest bearing easy-access savings deal.The best easy-access savings account currently pays 2.1 per cent. On a £20,000 deposit that would mean £420 in interest over the course of a year.What other savings draws are worth considering?Halifax Savers Prize Draw Halifax current account customers can register through online banking or by visiting a local branch for its savings draw.Each month over 1,600 savings customers in the Halifax draw are randomly selected to win money – three of the prizes being worth £100,000.However, there is one barrier to overcome as they’ll need to hold £5,000 or more in savings for a whole month to be entered into the following month’s prize draw.The £5,000 can be made up of multiple pots across any Halifax savings account including cash Isas, although children’s accounts are excluded.Nationwide’s Member Prize DrawNationwide members benefit from a monthly prize draw split into 8,008 prizes, with one worth £100,000, two worth £25,000, five worth £10,000 and the rest all worth £100.Unlike, with Halifax, Nationwide members are automatically opted in, so as long as you hold a mortgage, savings account or current account with Nationwide, there is nothing to do.Nationwide currently has around 14million members eligible for the Prize Draw.Yorkshire Building Society Make Me a Saver accountThis regular savings account pays 1.65 per cent interest and instant access to savings without penalty whilst offering 10 £1,500 prizes each month.To be entered into one of the prize draws, customers need to deposit money into the account and increase the balance by at least £50 each month.The account also allows for unlimited instant withdrawals without loss of interest.A total of eleven prize draws will take place once each month between March 2022 and January 2023 with the account maturing on 31 January 2023.It’s worth noting that the account limit savers to a maximum deposit of £150 per month, meaning a total of £1,800 can be saved over 12 months.Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence. .

Premium Bonds have been a popular product for UK savers for more than 65 years.Although the majority of prizes are worth £25, Premium Bond holders are always in with a distant chance of winning one of the two £1million monthly jackpot prizes. There are also ten £100,000 prizes and 19 prizes worth £50,000.In May, NS&I increased the Premium Bond underlying prize fund rate from 1 per cent to 1.4 per cent boosting the chances of its 21million savers bagging a monthly prize.It means the odds of each £1 Premium Bond number winning a prize has now changed from 34,500 to 1 to 24,500 to 1. Chip is unable to give the odds of winning just yet as its only in the first month of the account being live, although it says in future, it hopes to share this once it collects more data. However, needless to say, the more savers deposit the more entries the will have in the prize draw each month.One other factors for savers to consider is the fact that Premium Bond prizes are tax free whilst Chip’s prizes could incur tax depending on whether they exceed a person’s annual tax free allowance. Ultimately, there is no guarantee of winning anything with these prize draws. Savers looking for guaranteed returns whilst retaining access to their cash may do better to consider an interest bearing easy-access savings deal.The best easy-access savings account currently pays 2.1 per cent. On a £20,000 deposit that would mean £420 in interest over the course of a year.What other savings draws are worth considering?Halifax Savers Prize Draw Halifax current account customers can register through online banking or by visiting a local branch for its savings draw.Each month over 1,600 savings customers in the Halifax draw are randomly selected to win money – three of the prizes being worth £100,000.However, there is one barrier to overcome as they’ll need to hold £5,000 or more in savings for a whole month to be entered into the following month’s prize draw.The £5,000 can be made up of multiple pots across any Halifax savings account including cash Isas, although children’s accounts are excluded.Nationwide’s Member Prize DrawNationwide members benefit from a monthly prize draw split into 8,008 prizes, with one worth £100,000, two worth £25,000, five worth £10,000 and the rest all worth £100.Unlike, with Halifax, Nationwide members are automatically opted in, so as long as you hold a mortgage, savings account or current account with Nationwide, there is nothing to do.Nationwide currently has around 14million members eligible for the Prize Draw.Yorkshire Building Society Make Me a Saver accountThis regular savings account pays 1.65 per cent interest and instant access to savings without penalty whilst offering 10 £1,500 prizes each month.To be entered into one of the prize draws, customers need to deposit money into the account and increase the balance by at least £50 each month.The account also allows for unlimited instant withdrawals without loss of interest.A total of eleven prize draws will take place once each month between March 2022 and January 2023 with the account maturing on 31 January 2023.It’s worth noting that the account limit savers to a maximum deposit of £150 per month, meaning a total of £1,800 can be saved over 12 months.Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence. .