A screen displays trading informations for stocks on the floor of the New York Stock Exchange (NYSE) in New York City, U.S., June 27, 2022. REUTERS/Brendan McDermidRegister now for FREE unlimited access to Reuters.comNEW YORK, July 15 (Reuters) – Fears of a potential economic slowdown are clouding the outlook for value stocks, which have outperformed broader indexes this year in the face of surging inflation and rising interest rates.Value stocks – commonly defined as those trading at a discount on metrics such as book value or price-to-earnings – have typically underperformed their growth counterparts over the past decade, when the S&P 500’s (.SPX) gains were driven by tech-focused giants such as Amazon.com Inc (AMZN.O) and Apple Inc (AAPL.O).That dynamic shifted this year, as the Federal Reserve kicked off its first interest rate-hike cycle since 2018, disproportionately hurting growth stocks, which are more sensitive to higher interest rates. The Russell 1000 value index (.RLV) is down around 13% year-to-date, while the Russell 1000 growth index (.RLG) has fallen about 26%.Register now for FREE unlimited access to Reuters.comThis month, however, fears that the Fed’s monetary policy tightening could bring on a U.S. recession have shifted the momentum away from value stocks, which tend to be more sensitive to the economy. The Russell value index is up 0.7% in July, compared with a 3.4% gain for its growth-stock counterpart.”If you think we are in a recession or are going into a recession, that does not necessarily … work to the advantage of value stocks,” said Chuck Carlson, chief executive at Horizon Investment Services.The nascent shift to growth stocks is one example of how investors are adjusting portfolios in the face of a potential U.S. economic downturn. BofA Global Research on Thursday cut its year-end target price for the S&P 500 to 3,600 from 4,500 previously and became the latest Wall Street bank to forecast a coming recession. read more The index closed at 3,863.16 on Friday and is down 18.95% this year.Corporate earnings arriving in force next week will give investors a better idea of how soaring inflation has affected companies’ bottom lines, with results from Goldman Sachs , Johnson & Johnson (JNJ.N) and Tesla among those on deck.For much of the year, value stocks benefited from broader market trends. Energy shares, which comprise around 7% of the Russell 1000 value index, soared over the first half of 2022, jumping along with oil prices as supply constraints for crude were exacerbated by Russia’s invasion of Ukraine.But energy shares along with crude prices and other commodities have tumbled in recent weeks on concerns that a recession would sap demand.A recession also stands to weigh on bank stocks, with a slowing economy hurting loan growth and increasing credit losses. Financial shares represent nearly 19% of the value index. read more An earnings beat from Citigroup, however, buoyed bank shares on Friday, with the S&P 500 banks index (.SPXBK)gaining 5.76%.At the same time, tech and other growth companies also tend to have businesses that are less cyclical and more likely able to weather a broad economic slowdown.”People pay a premium for growth stocks when growth is scarce,” said Burns McKinney, portfolio manager at NFJ Investment Group.JPMorgan analysts earlier this week wrote they believe growth stocks have a “tactical opportunity” to make up lost ground, citing cheaper valuations after this year’s sharp sell-off as one of the reasons.Value stock proponents cite many reasons for the investing style to continue its run.Growth stocks are still more expensive than value shares on a historical basis, with the Russell 1000 growth index trading at a 65% premium to its value counterpart, compared to a 35% premium over the past 20 years, according to Refinitiv Datastream.Meanwhile, earnings per share for value companies are expected to rise 15.6% this year, more than twice the rate of growth companies, Credit Suisse estimates.Data from UBS Global Wealth Management on Thursday showed value stocks tend to outperform growth stocks when inflation is running above 3% – around a third of the 9.1% annual growth U.S. consumer prices registered in June. read more Josh Kutin, head of asset allocation, North America at Columbia Threadneedle, believes a possible U.S. recession in the next year would be a mild one, leaving economically sensitive value stocks primed to outperform if growth picks up.”If I had to pick one, I’d still pick value over growth,” he said. “But that conviction has come down since the start of the year,” Kutin said.Register now for FREE unlimited access to Reuters.comReporting by Lewis Krauskopf, additional reporting by David Randall and Ira Iosebashvili; Editing by Ira Iosebashvili and Richard ChangOur Standards: The Thomson Reuters Trust Principles. .

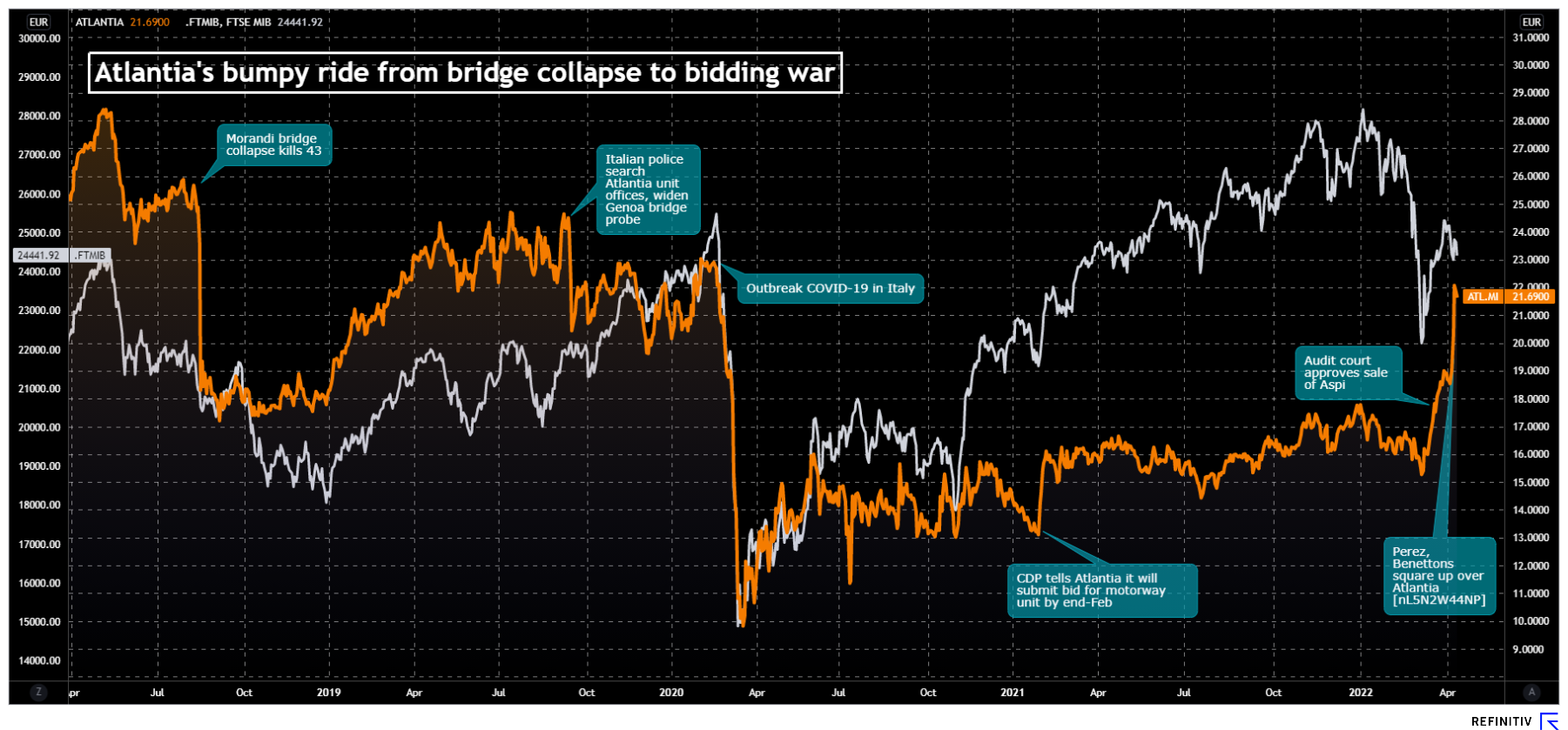

Atlantia’s share performanceEdizione and Blackstone want to delist Atlantia to shield it from the appetite of rival suitors, who approached the Benettons last month with a proposal to buy the group and hand over Atlantia’s motorway concessions to Perez.GIP, Brookfield and the Spanish tycoon are in a ‘wait and see’ mode after the Benetton family and Atlantia’s long-time investors CRT and GIC rebuffed their offer, sources have said.The takeover offer comes as Atlantia prepares to pocket 8 billion euros from the sale of the group’s Italian motorway unit, a deal aimed at ending a political dispute triggered by the 2018 collapse of a motorway bridge.It also puts the spotlight on Alessandro Benetton, 58, who was appointed chairman of Edizione earlier this year, tightening the family’s grip on its investments.After parting ways with its Autostrade per l’Italia, Atlantia will continue to run airports in Italy and France, motorways in Europe and Latin America and digital toll payment company Telepass.The Italian government so far has been silent on the latest developments, but it has special vetting ‘golden’ powers over strategic assets, such as the country’s airports and their ownership.($1 = 0.9184 euro)Register now for FREE unlimited access to Reuters.com

Atlantia’s share performanceEdizione and Blackstone want to delist Atlantia to shield it from the appetite of rival suitors, who approached the Benettons last month with a proposal to buy the group and hand over Atlantia’s motorway concessions to Perez.GIP, Brookfield and the Spanish tycoon are in a ‘wait and see’ mode after the Benetton family and Atlantia’s long-time investors CRT and GIC rebuffed their offer, sources have said.The takeover offer comes as Atlantia prepares to pocket 8 billion euros from the sale of the group’s Italian motorway unit, a deal aimed at ending a political dispute triggered by the 2018 collapse of a motorway bridge.It also puts the spotlight on Alessandro Benetton, 58, who was appointed chairman of Edizione earlier this year, tightening the family’s grip on its investments.After parting ways with its Autostrade per l’Italia, Atlantia will continue to run airports in Italy and France, motorways in Europe and Latin America and digital toll payment company Telepass.The Italian government so far has been silent on the latest developments, but it has special vetting ‘golden’ powers over strategic assets, such as the country’s airports and their ownership.($1 = 0.9184 euro)Register now for FREE unlimited access to Reuters.com